Nila Kartika Wati

Nila Kartika Wati The Capital Catalyst: Navigating the Complex Landscape of Modern Franchise Financing

By [Your Publication Name] Staff

In the current economic climate, franchising remains one of the most resilient engines of the global economy. Built on the foundation of proven systems, established branding, and rigorous operational playbooks, the model offers a shortcut to entrepreneurship that independent startups rarely enjoy. However, a widening chasm has emerged between operators who successfully scale to dozens of units and those whose ambitions stall at a single storefront.

The determining factor is rarely the quality of the product or the dedication of the staff; rather, it is the strategic mastery of access to capital. As the financial sector moves deeper into an era of specialized lending and tighter credit requirements, understanding the alchemy of franchise financing has become the most critical skill set for the modern operator.

Main Facts: The New Underwriting Paradigm

Historically, securing a business loan was a matter of presenting a decent credit score and a few years of tax returns. Today, the landscape is significantly more granular. Lenders are no longer passive providers of funds; they are sophisticated analysts of unit economics and brand longevity.

According to industry experts, including Christopher Cornella, Vice President of Business Development at US Medical Funding, lenders are now evaluating opportunities through a multi-dimensional lens. This includes:

- Brand Velocity and Stability: Lenders analyze the franchisor’s litigation history, store closure rates, and the strength of the corporate support system.

- Real-Time Unit Economics: Beyond high-level revenue, banks are scrutinizing EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) at the individual store level to ensure the business can withstand inflationary pressures on labor and goods.

- The "Operator Alpha": There is an increasing premium placed on the "operator experience." A seasoned franchisee with a track record of running three successful units is viewed as a significantly lower risk than a high-net-worth individual entering the space for the first time.

- Territory Integrity: Lenders are looking at geographic saturation and whether a specific territory has the demographic runway to support the projected growth.

For the franchisee, the "Capital Gap" is the distance between the total project cost—including often-overlooked working capital—and the available liquid assets. Closing this gap requires a sophisticated blend of Small Business Administration (SBA) loans, conventional bank financing, and equipment leasing.

Chronology: The Lifecycle of Franchise Capital

The financial needs of a franchise business evolve through distinct stages, each requiring a different strategy and a different conversation with lenders.

Phase 1: The Startup and The Leap of Faith

In the beginning, financing is predicated on "projections" rather than "performance." Because there is no historical cash flow to audit, lenders focus heavily on the borrower’s personal financial health and the franchisor’s track record. This is where SBA 7(a) loans are most prevalent, providing the 75% to 90% financing necessary to get the doors open. The "chronology" here is often a race against the clock: securing the lease, paying the franchise fee, and beginning construction before the initial capital reserves are depleted by "soft costs."

Phase 2: The Stabilization Period

Once the unit is open, the focus shifts to liquidity management. Many operators fail in the first 12 to 18 months not because the business isn’t profitable, but because the "ramp-up" period was longer than anticipated. During this phase, equipment financing becomes a vital tool, allowing operators to keep cash in the bank for payroll and marketing while paying off high-cost assets (like ovens, medical lasers, or gym equipment) over five to seven years.

Phase 3: The First Expansion (The "Chasm")

Moving from one unit to two or three is the most dangerous transition in franchising. The operator must move from being an "owner-operator" to a "multi-unit manager." Lenders watch this transition closely. If the first unit’s cash flow dips because the owner is distracted by the second unit’s construction, future funding may dry up. Successful expansion during this period usually involves refinancing the original debt to improve cash flow for the next project.

Phase 4: The Enterprise Scale

For operators with five or more units, the conversation changes from "loans" to "credit facilities." Large-scale franchisees often secure development lines of credit, allowing them to acquire or build new locations with pre-approved terms. At this stage, the business is treated as a corporate entity, and financing is based on the aggregate health of the entire portfolio.

Supporting Data: The Efficiency of the Franchise Model

Lenders favor franchises because the "failure rate" is statistically lower than that of independent businesses. Data from the International Franchise Association (IFA) suggests that franchised businesses have a higher five-year survival rate compared to independent startups. This "safety net" allows for more aggressive lending terms.

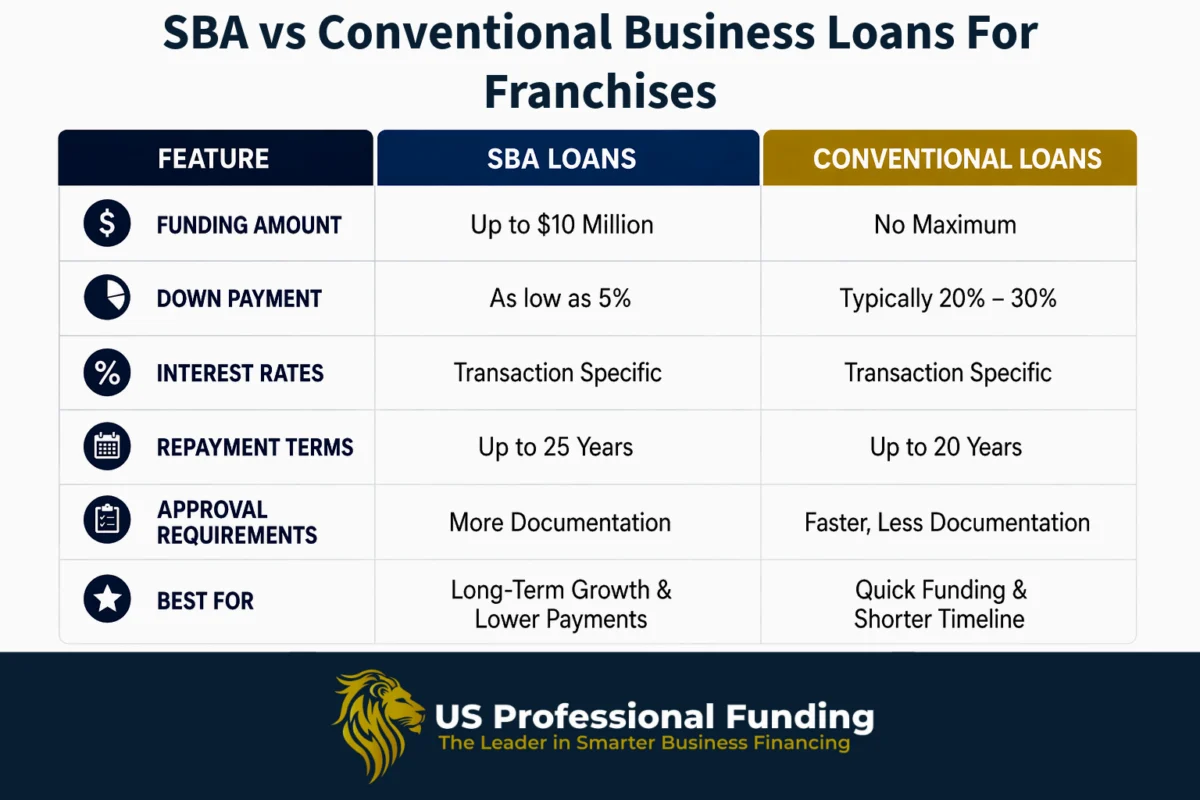

SBA 7(a) vs. Conventional Lending

| Feature | SBA 7(a) Loans | Conventional Bank Loans |

|---|---|---|

| Down Payment | Typically 10% – 15% | Typically 20% – 30% |

| Collateral | Often requires personal residence | Focuses on business assets/real estate |

| Terms | Up to 10 years (25 for RE) | 5 to 7 years (typically) |

| Speed | 60 to 90 days | 30 to 45 days |

| Flexibility | Higher (Government guaranteed) | Lower (Bank takes 100% risk) |

Furthermore, the "Franchise Registry"—a list of brands whose FDDs (Franchise Disclosure Documents) have been vetted—allows for expedited SBA processing. Brands on this registry are viewed as "pre-vetted," significantly reducing the administrative burden on the lender and the borrower.

Official Responses: Insights from the Front Lines

Christopher Cornella, a veteran in the commercial financing space, emphasizes that the most common pitfall for franchisees is a narrow focus on interest rates.

"The cheapest money is not always the best money," Cornella notes. "A slightly higher interest rate on a loan that offers an interest-only period during construction, or one that doesn’t have a punishing prepayment penalty, can be worth far more to an operator’s long-term health than a low-rate loan that ties up every dollar of liquidity."

Cornella’s experience at US Medical Funding and US Professional Funding highlights a growing trend: the rise of industry-specific lending. For example, medical and dental franchises are often viewed differently than QSR (Quick Service Restaurant) franchises. Medical concepts may have higher equipment costs but more predictable, "sticky" customer bases, leading to different amortization schedules.

Lenders are also increasingly vocal about the "Working Capital Trap." They report that a primary reason for loan defaults is not the debt itself, but the lack of "breathing room." Sophisticated lenders are now insisting that franchisees include six to nine months of operating expenses in their initial loan request, rather than trying to "lean-start" the business.

Implications: The Strategic Future of Growth

The implications of this evolving financing landscape are profound for the future of the industry.

First, we are seeing the "Professionalization of the Franchisee." The days of the "hobbyist" owner are fading. To secure the capital required for modern build-outs—which have increased in cost due to supply chain shifts and labor shortages—operators must present professional-grade financial reporting and a clear "succession plan" for their management teams.

Second, Strategic Capitalization is becoming a competitive advantage. In a crowded market, the operator who can secure 90% financing with a 10-year term has more cash on hand to out-market and out-hire the competitor who is struggling with a 5-year conventional loan and high monthly payments.

Finally, the Consolidation of Brands is likely to continue. Lenders are gravitating toward "Tier 1" brands with proven resilience during economic downturns. This makes it harder for new, unproven franchisors to gain traction, but it also ensures that the capital flowing into the sector is supporting the most robust business models.

Conclusion

Financing is the heartbeat of the franchise industry. It is the tool that transforms a single successful store into a regional empire. However, as the market becomes more competitive and lenders more discerning, the "guesswork" of borrowing must be replaced by a strategic, data-driven approach.

For the franchisee, the path to scale is paved with more than just hard work; it is built on a foundation of liquidity, brand strength, and a deep understanding of how to make a lender say "yes." As Christopher Cornella and other industry leaders suggest, those who master the art of the "capital stack" will be the ones who define the next decade of American business growth.

0 Comment